The term “non-qualified” on a credit card processing statement can mean a number of things. But whatever reason it’s there, it usually means you paid more than you could have.

Non-qualified charges indicate expensive transaction costs for you. There are two main reasons for them: your processor charged you a non-qualified rate, or your transactions “downgraded” to Visa’s non-qualified interchange category.

It’s easy to confuse Visa’s non-qualified interchange with the non-qualified rates from your processor. To understand the difference, let’s take a look at both situations and how you can fix them if they happen to you.

Overview of Differences

The main difference between Visa’s non-qualified interchange rate and a credit card processor’s non-qualified rate is that Visa’s is fixed and the same for every business. Visa sets the interchange rates. On the other hand, a credit card processor determines their own “non-qualified” rate, including when to charge it. It can vary for every business. Let’s dig into that a little more.

Processor’s Non-Qualified Charges

Non-qualified rates on the credit card processor’s side indicate tiered pricing, an expensive and opaque pricing model widely used in credit card processing. I’ve written extensively about tiered pricing and why it is bad for businesses, but to sum up: with transparent, cost-effective pricing models, the processor will pass along the real interchange costs that Visa sets. You’ll pay that price, plus the processor’s fee.

With tiered pricing, the processor obscures that. They will create “tiers” to charge you. It’s common to see three tiers: qualified, mid-qualified, and non-qualified. Each tier has a rate associated, and the processor groups all of the interchange categories into those tiers. A lower cost category at the interchange level could be routed to the processor’s highest-cost “non-qualified” tier, completely at their discretion. The processor chooses which categories go to which tiers and can change it at any time. The processor’s non-qualified rate will typically be higher than the interchange-level non-qualified rate.

Visa’s Non-Qualified Interchange Rate

The Visa “non-qualified” rate comes into play at the interchange level. It is a specific interchange category among hundreds. If you’re not familiar with interchange, you can read our intro: Interchange Rates and Fees.

Interchange is a core component of credit card processing costs, with Visa setting the rates for each interchange category. Your processor has no control over the interchange rates. Every card payment you take at your business will get routed to one of those interchange categories. Which one depends on factors like type of card, acceptance method, industry, and more.

Non-qualified interchange is a specific category for transactions that don’t meet criteria for lower-cost categories.

Common Reasons to Downgrade to Visa Non-Qualified

There are several reasons a transaction may “downgrade” to the Visa Non-Qualified interchange category. Typically, it’s any situation that causes a transaction to be riskier than it needed to be. For example, a business that doesn’t use an EMV credit card machine and instead relies on magstripe swiping could see their transactions downgrade to Visa Non-Qualified. A business that sets up credit card processing as a card-present business but manually keys in transactions may also see downgrades to non-qualified.

In these situations, the transactions are viewed as riskier. The Non-Qualified category has a higher rate to offset the risk of the transaction.

When Non-Qualified isn’t a Downgrade

There are limited situations where Visa’s non-qualified interchange category isn’t a downgrade, it’s actually the best possible category a transaction could qualify for. This primarily affects “non-secure” online transactions and high-risk businesses.

Visa doesn’t explicitly detail what constitutes a “non-secure” transaction in its publicly available information, but typically it would include things like not using 3DSecure technology, as well as engaging in risky online processing behavior such as accepting transactions despite billing address mismatches or AVS warnings.

Due to the higher risk associated with those transactions, they are not eligible for lower-cost interchange categories. The best they can do is the Non-Qualified interchange category.

This is also true for some “high-risk” businesses. Due to the nature of their industry or business profile, such businesses are classed as high risk and not eligible for lower cost categories. Instead, the transactions will receive the Non-Qualified interchange category and associated rate.

What to do about Non-Qualified Charges

How you proceed depends on whether you’re seeing non-qualified charges at the interchange level (Visa’s charges) or as part of a processor’s tiered pricing.

It used to be easy to spot tiered pricing through the use of non-qualified charges, as there was no interchange category called “non-qualified.” Visa changed that, introducing the non-qualified category and muddying the waters.

If you see a non-qualified charge on your statement, you can determine if it matches Visa’s non-qualified interchange rate. (Currently 3.15% + 10 cents per transaction for consumer credit, but subject to change at Visa’s discretion.)

Interchange Non-Qualified

In the statement below, this business is on a competitive interchange-plus pricing model. If this business receives a non-qualified charge, it should be at the interchange level.

In this statement, the non-qualified charge is listed with other interchange fees, and doing the math shows us it is in fact charged at 3.15% + 10 cents per transaction.

There were 17 total non-qualified transactions. That means we need to multiply 17 by 10 cents (the per-transaction fee), totalling $1.70.

Now, we figure out 3.15% of the total volume, $9,566.72, which comes out to $301.3517.

We then add $1.70, coming out to $303.0517, which this processor apparently rounded up to $303.06. That’s the number that we see the processor charged, so it was passed through at the real interchange cost that Visa set.

That means the best thing this business can do is investigate why they had 17 transactions that went to the “non-qualified” interchange category. There may be steps the business can take with their processor to adjust how they accept those cards to minimize non-qualified transactions, but ultimately the processor cannot control this rate. Still, in this situation it can be worthwhile to contact your processor to attempt to address the non-qualified transactions. CardFellow clients can call us for help.

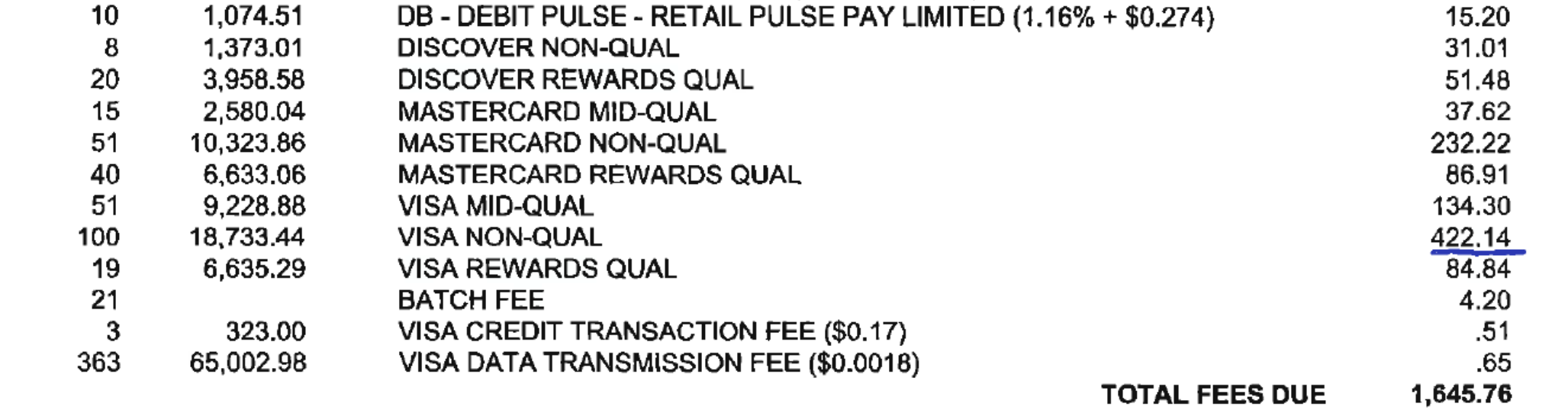

Processor’s Non-Qualified Rates

If you’re on tiered pricing, the processor may or may not list the interchange categories your transactions were charged to. The non-qualified line will still be there, but if you do the math, it likely doesn’t come out to 3.15% + 10 cents.

Additionally, you may see “qualified” and “mid-qualified” (sometimes abbreviated qual and mqual) elsewhere on the statement which indicate tiered pricing.

In the statement above, you can see Non-Qual, Mid-Qual, and Qual rates listed. At least for now, Visa does not have “mid-qualified” and “qualified” interchange categories.

The only way to fight processor non-qualified rates is to switch from tiered pricing. You can find competitive interchange plus solutions right here in the CardFellow marketplace. It’s free and private, letting you see real pricing from multiple processors with no obligation. Give it a try at www.cardfellow.com.