Visa’s Supermarket Credit interchange is charged differently depending on two different factors: the type of credit card used and the “tier” of the supermarket.

Note that this does not apply to debit and prepaid cards used at a supermarket. Those card types have their own interchange (CPS Supermarket), which we cover in this article: Visa CPS Supermarket.

Let’s take a look at the eligibility requirements for the categories and what you can expect to pay if you’re running a supermarket and accepting Visa credit cards.

Supermarket Tiers

As noted in the introduction, there are two key factors that affect the interchange rates your business will be charged. One is the supermarket’s “tier.” In Visa’s interchange schedule, the card company defines the threshold for the supermarket tiers. As of 2023, those tiers are as follows:

| Supermarket Tier | Minimum Transactions | Minimum Volume |

| Tier 0 | 370 million | $19.6 billion |

| Tier I | 132.5 million | $10.65 billion |

| Tier II | 72.5 million | $4.20 billion |

| Tier III | 16.5 million | $950 million |

Note that other factors also apply – supermarkets must be PCI compliant, and have a maximum ratio for disputes of 0.020% or less.

Supermarket Interchange Rates

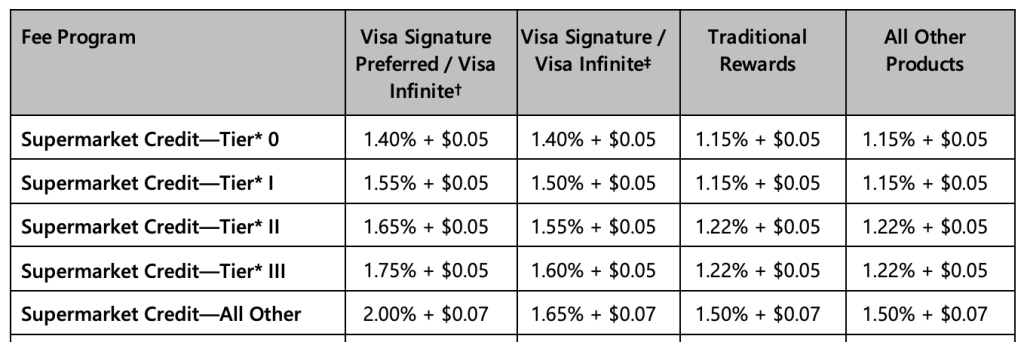

Once you know the tier for the supermarket, you can review the interchange table for Supermarket Credit, which includes rows for different types of Visa credit cards:

As you can see, the lower the tier, the better the rates in most cases.

These rates come directly from Visa’s published interchange schedule. However, rates are subject to change at Visa’s discretion.

Keep in mind that these are not the only rates that can apply to supermarkets. If you don’t meet requirements for one of the above categories, your transaction can “downgrade” to a more expensive category.

Check out our article on interchange rates and fees for more information.

Supermarket Credit Interchange Criteria

Aside from the supermarket tier, there are other criteria that must be met in order to receive the Supermarket Credit rates noted above. There are several eligibility requirements to receive CPS Supermarket interchange rates.

Business is a Supermarket

No surprise here – to be eligible for supermarket credit interchange rates, your business has to be, well, a supermarket. More importantly, it must be noted through your merchant category code (MCC), which your processor sets up. Merchant Category Code 5411 (Supermarkets) determines eligibility for this category.

If you run a supermarket but aren’t receiving supermarket credit interchange, it’s possible you’re set up with an incorrect MCC. In that case, check with your processor to resolve it.

Credit Card Only

The rates noted above only apply to Visa credit cards. They do not apply to prepaid cards or debit cards, which instead have their own categories called CPS Supermarket – Debit and CPS Supermarket – Prepaid.

Card Present Transactions

To qualify, the transaction must be run through a credit card machine, that is, be “card-present.” Card-present transactions include magstripe swipes, EMV chip card “dips,” and contactless payment “ta[s.” Any other method of entering the card, including keying in the card details, is a card-not-present transaction even if the card was literally at the store.

Settlement Time

In addition to the other criteria noted, the transaction must be settled within 24 hours of the authorization. Many businesses “batch” once per day to strike a balance of meeting settlement times and not causing onerous constant batching. Many credit card machines and POS systems allow you to set automatic batching at particular intervals.)

If you choose to manually batch transactions, make sure transactions are settled within 24 hours to avoid expensive “downgrade” interchange categories.

Supermarket Credit on Monthly Statements

Depending on your processor, you may see Supermarket Credit interchange listed with one of its abbreviations or aliases.

Those include:

- VI SUPRMKT

- SUPRMKT

And other variations.

However, not all processors provide interchange detail with your monthly statements. Aggregators like Square only provide short form statements that don’t include interchange detail. Other processors may require you to request the full interchange detail. It’s worth making sure that you’re being charged what you should be, so be sure to request interchange detail. You can also sign up at CardFellow for help understanding your statement and comparing to other processors.