What is Surcharging?

Surcharging, defined as adding a fee to purchases made with a credit card, was prohibited by the card brands (Visa and Mastercard) until a class action lawsuit in 2013. The idea is that a business can defray the costs of accepting credit cards by charging the consumers that choose to pay with a credit card. Consumers that pay with cash would not receive a fee. This is (subtly) different than cash discounting, where consumers who pay with cash receive a discount on the price as a perk for not using a credit card. While the end result is the same (credit card users pay more than cash users) the distinction has been important for implementing compliant surcharge and cash discount programs. It also has some effect on customer perception, as people respond positively to a discount and negatively to added fees.

This is (subtly) different than cash discounting, where consumers who pay with cash receive a discount on the price as a perk for not using a credit card. While the end result is the same (credit card users pay more than cash users) the distinction has been important for implementing compliant surcharge and cash discount programs. It also has some effect on customer perception, as people respond positively to a discount and negatively to added fees.

Why was Surcharging Prohibited?

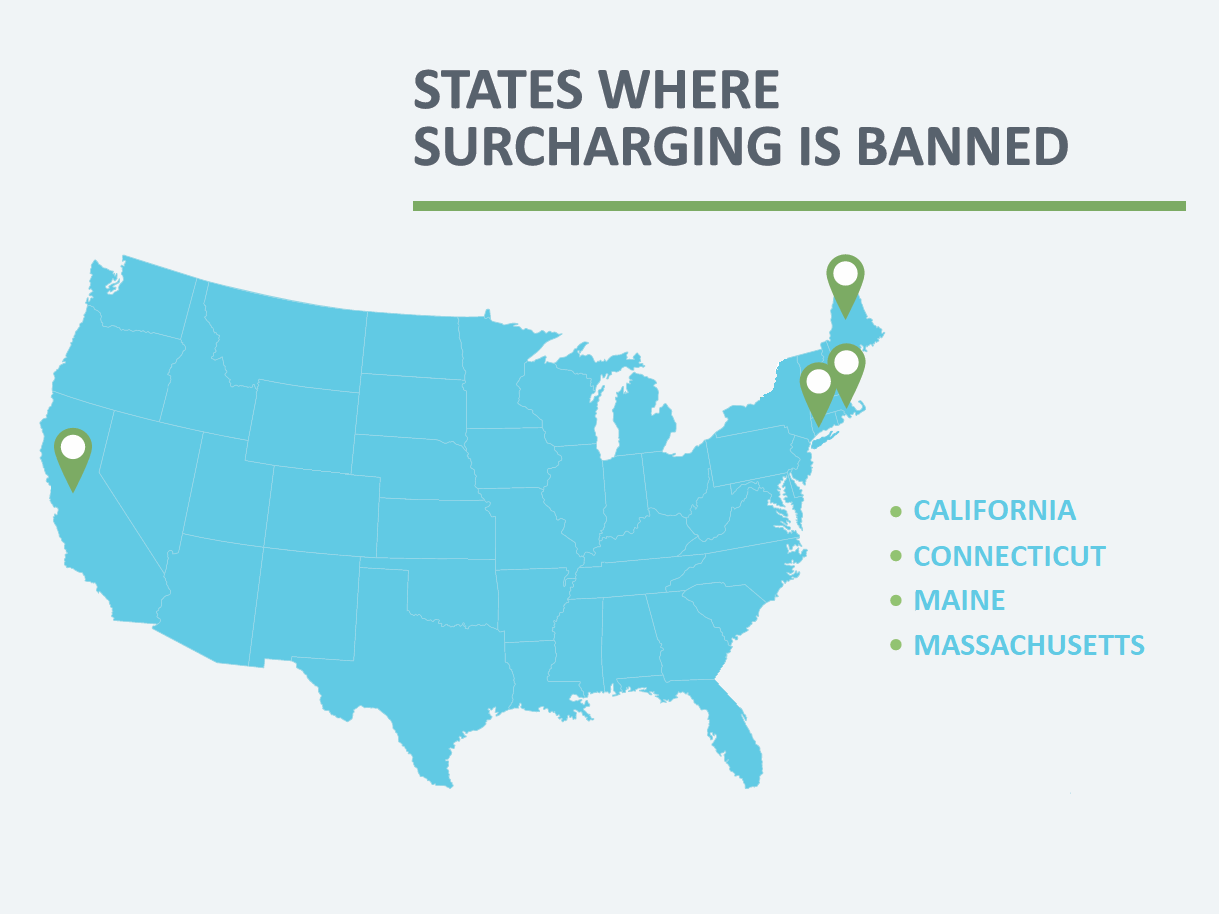

Up until 2013, Visa and Mastercard prohibited surcharging simply because it could dissuade customers from using their cards. Visa and Mastercard have a vested interest in customers using credit cards as often as possible, because both companies make money through the assessment fees that are part of credit card transaction costs that businesses pay. The card brands didn’t want consumers to have second thoughts about using their cards to avoid extra fees. The turning point came in 2013 when a class action lawsuit resulted in a settlement agreement between businesses and the card companies. The settlement allowed businesses to impose surcharges on credit card transactions. However, there were requirements and stipulations regarding how much could be charged as well as required disclosures prior to charging the fees. Additionally, state laws played a role, with some prohibiting surcharges regardless of the new rules from Visa and Mastercard. You can get more details on that in our article on credit card surcharges.

You can get more details on that in our article on credit card surcharges.

Adoption of Surcharge Programs

Credit card surcharging and cash discounting was slow to take hold in the years immediately following the class action lawsuit. This is not surprising, as it can take awhile for processing companies to create and market new programs that cater to new concepts such as surcharging. Once that's done, it also can take time for business owners to research the programs and ultimately sign up. However, according to a press release quoting the J.D. Power 2025 U.S. Merchant Services Satisfaction Study released in mid-January, 34% of businesses now add surcharges to transactions paid by credit card. New or smaller businesses are the most likely to implement surcharges. So what about the consumer? The same press release states that 41% of credit card users say they have decided not to use a card due to a surcharge. It’s unclear from the release if those consumers simply paid with cash instead or if they declined to continue the transaction.Should You Surcharge?

What does this mean for you? It depends. As noted above, a customer deciding not to use a card may simply mean that they choose to pay with cash instead, with minimal impact on perception or their purchase. However, there’s some evidence that people spend more with credit cards than they do when they pay with cash. Nerdwallet has a good roundup citing specific examples, including one study by the Federal Reserve Bank of Boston that found that in 2016, the average cash transaction was $22 vs a whopping $112 for non-cash transactions. Granted, that was several years ago, but newer information still bears out the idea that cash transactions tend to be smaller than non-cash. Chase Bank cites a 2023 study conducted by Forbes Advisor saying that 52% of people surveyed report being more likely to make an “impulse buy” when using a card, compared to only 24% of people who use cash. 58% stated that credit cards would be the most likely payment method that would cause them to spend more money. Why? Theories suggest that psychologically, we tend to view cash as “real” money, with immediate implications when we spend it. Credit card transactions don’t have any immediate “loss.” We don’t have to pay the bill until the following month (or later), making the transaction more nebulous. Handing over cold, hard cash makes us more aware of how much we are spending and may make us more carefully consider if it’s a necessary or good purchase. All of this means that it’s worth considering whether surcharging credit card transactions is more likely to make your customers reconsider their purchase or make a smaller purchase; both of which have negative effects on your bottom line.Considerations for Surcharging

Businesses that have a high likelihood of “impulse buys” may be particularly susceptible to losing sales if they put barriers to credit card usage, such as surcharges. Businesses with high ticket items may also see reluctance from buyers because surcharges are charged as a percentage of the sale and therefore will be higher on larger transactions. Additionally, less consumers carry cash at all, and when they do, may not carry large amounts of it. On the other hand, prominence of “shop small” campaigns and a desire to support local businesses has led to more consumers being aware of the costs of running a small business. Some consumers may be comfortable with additional fees for things like using a credit card since they know that small businesses face many challenges and want to support their favorite stores and restaurants. At the end of the day, you’ll need to make the call based on your customers, business type, competition, and location.Other Ways to Lower Processing Costs

Of course, before considering a surcharge or cash discount program, it’s worth determining if you’re overpaying for credit card processing in the first place. (Many businesses do!) We can help you with that - sign up for a free CardFellow account to quickly compare the best possible rates for your specific business. It’s private (no sales calls!) and no obligation. Start off armed with where your processing fees should be and you’ll be better equipped to determine if it’s time to consider surcharging or if you first need to secure better pricing. While the practice of adding a surcharge has become more common, it’s still up to you to decide what’s right for your business and your customers. Give us a call or sign up for a free account if you need help.

Ben Dwyer began his career in the processing industry in 2003 on the sales floor for a Connecticut‐based processor. As he learned more about the inner‐workings of the industry, rampant unethical practices, and lack of assistance available to businesses, he cut ties with his employer and started a blog where he could post accurate information about credit card processing. As the blog gained in popularity, Ben began directly assisting merchants in their search for a processor. Ben believes in empowering businesses by providing access to fair, competitive pricing, accurate information, and continued support. His dedication to transparency and education has made CardFellow a staunch small business advocate in the credit card processing industry.