Artificial intelligence, and ChatGPT in particular, is changing the way people research topics and get information. How does it hold up when it comes to credit card processing?

Note: CardFellow does not use ChatGPT or artificial intelligence to write blog posts. We are using ChatGPT for this article to go through the advice it may give when prompted to assist with comparing credit card processors.

Before we dive in, let’s briefly go over what ChatGPT actually does and how we approached this article on ChatGPT in credit card processing.

How does ChatGPT work?

ChatGPT is a type of computer model that was “trained” on text data from a variety of sources, including websites and books. The computer model “learns” patterns in written language, including grammar, but it doesn’t think like a person.

When a user asks ChatGPT a question, it tries to understand the context and provide an appropriate answer. It creates a logical response based on information it was already trained on. According to OpenAI, makers of ChatGPT, the information is from September 2021 and earlier. In some cases, ChatGPT can search the web for newer information, but it is not necessarily processing a response the same way and is more providing standard search results.

So is it possible that ChatGPT learned from CardFellow?

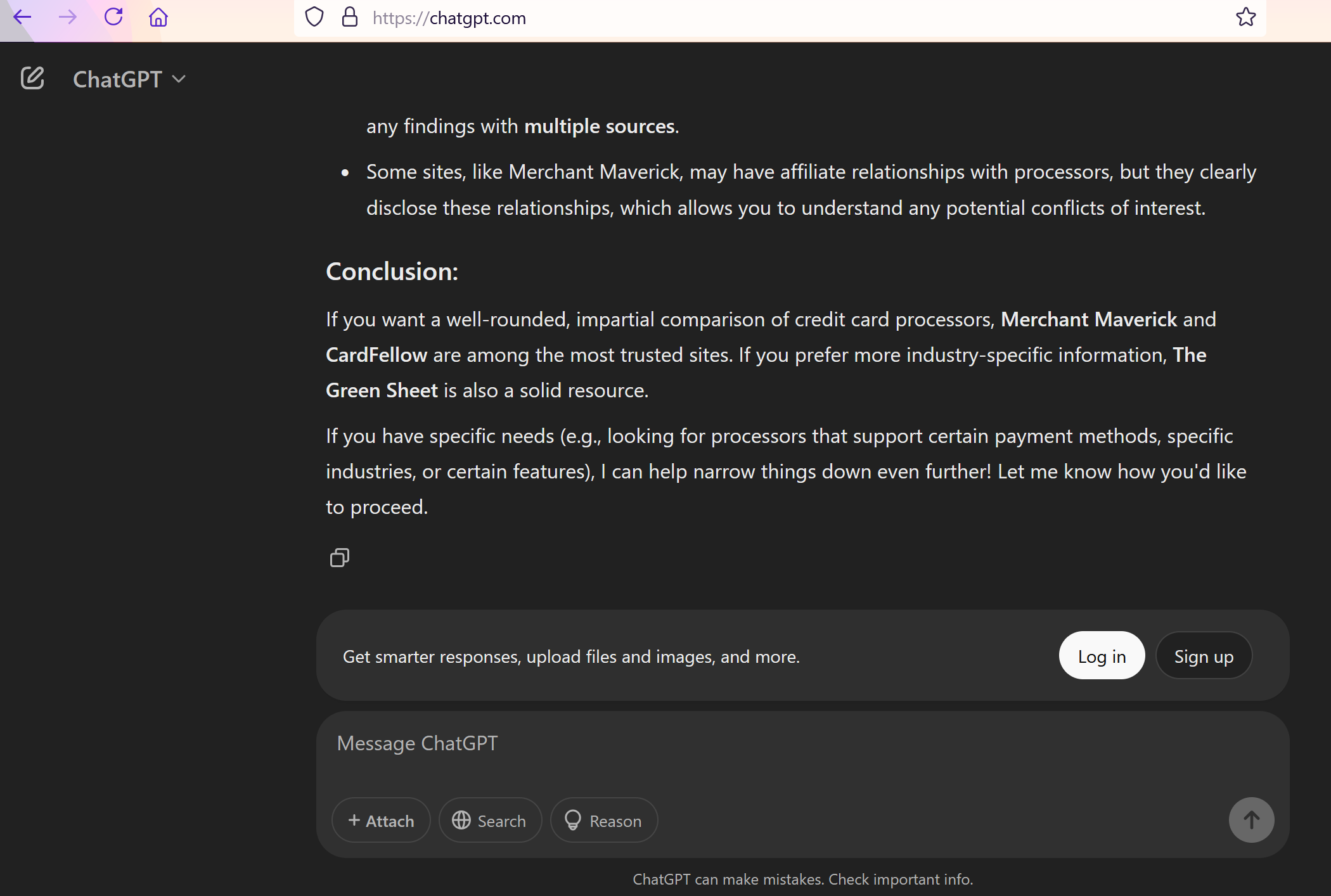

Yup. We don’t know for sure or how much, but ChatGPT is aware of CardFellow, as seen in this screenshot when I asked it for the most reliable website for getting unbiased information about credit card processing.

After referencing a review site and an industry publication, it pointed to CardFellow, mentioning our strength in offering transparent pricing comparisons and tools to help you find the best deal. It concluded that if you want a well-rounded, impartial comparison of credit card processors, we’re among the most trusted sites.

Of course, that also means that ChatGPT learned from other sources that may or may not have valid information. This is the big caveat about using ChatGPT in credit card processing and in general. It may learn from both good and poor sources of information, which can lead to potentially incorrect information. That’s also while you’ll see the disclaimer at the bottom of all queries stating, “ChatGPT can make mistakes. Check important info.”

Using ChatGPT for This Article

I approached this article with the intention of assessing whether ChatGPT is capable of providing accurate information about credit card processing, specifically assisting businesses with finding the right processor for their needs.

I worked up a fairly typical business profile: in-person transactions, $25,000 per month in credit card sales, and an average $100 transaction. I framed questions in ways that I’ve heard real customers ask over the years.

ChatGPT for Credit Card Processing

To start, I asked ChatGPT a common question that we see a lot here at CardFellow:

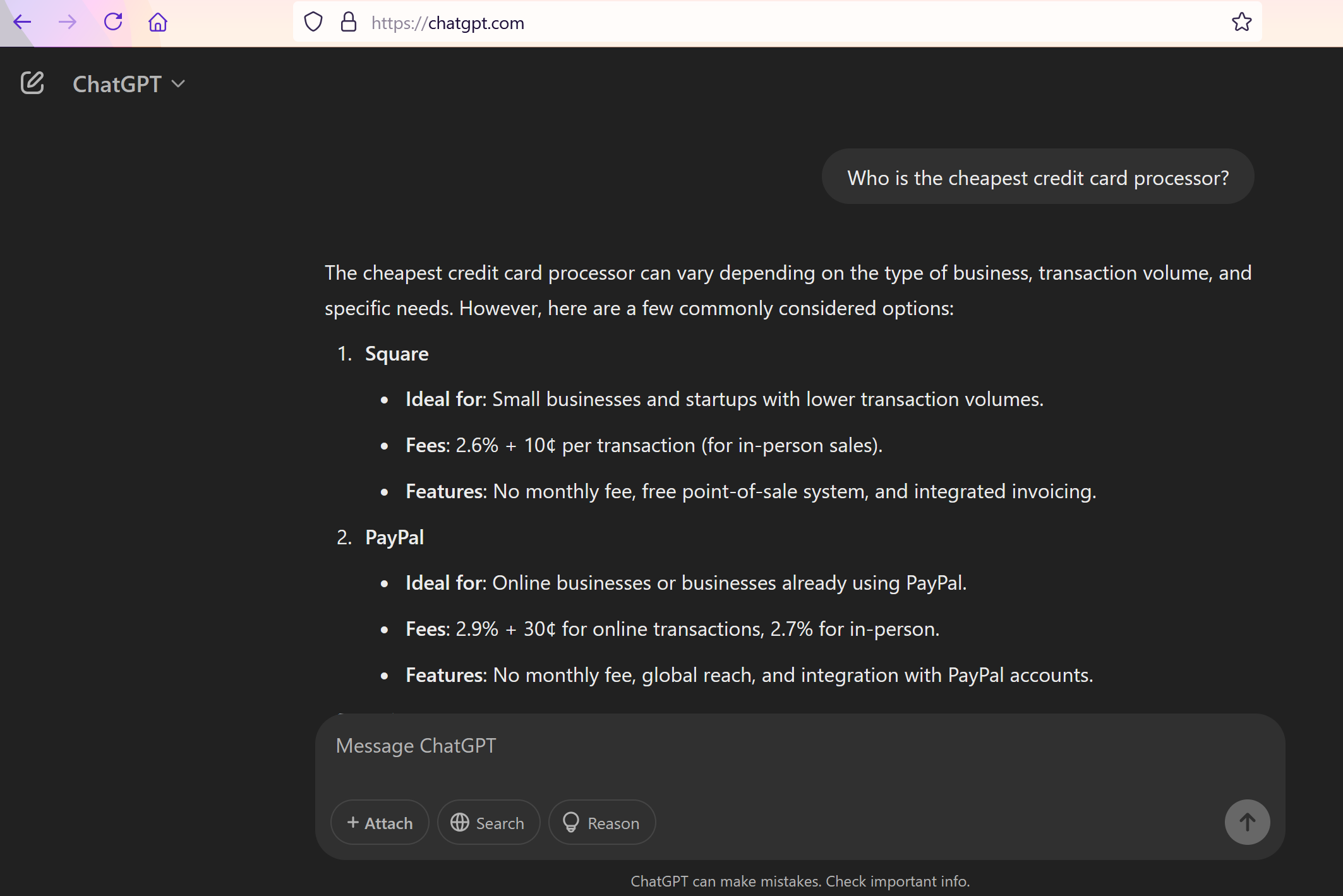

Who is the cheapest credit card processor?

ChatGPT’s reply started off promising, stating that the cheapest credit card processor can vary depending on the type of business, transaction, volume, and specific needs. This is all true. When you sign up for a CardFellow account to compare credit card processors, those are key pieces of information needed to help you find the right processing solution.

However, ChatGPT quickly veered into suggesting specific processors without knowing the details that it stated off the bat would affect the cheapest option. Strike 1.

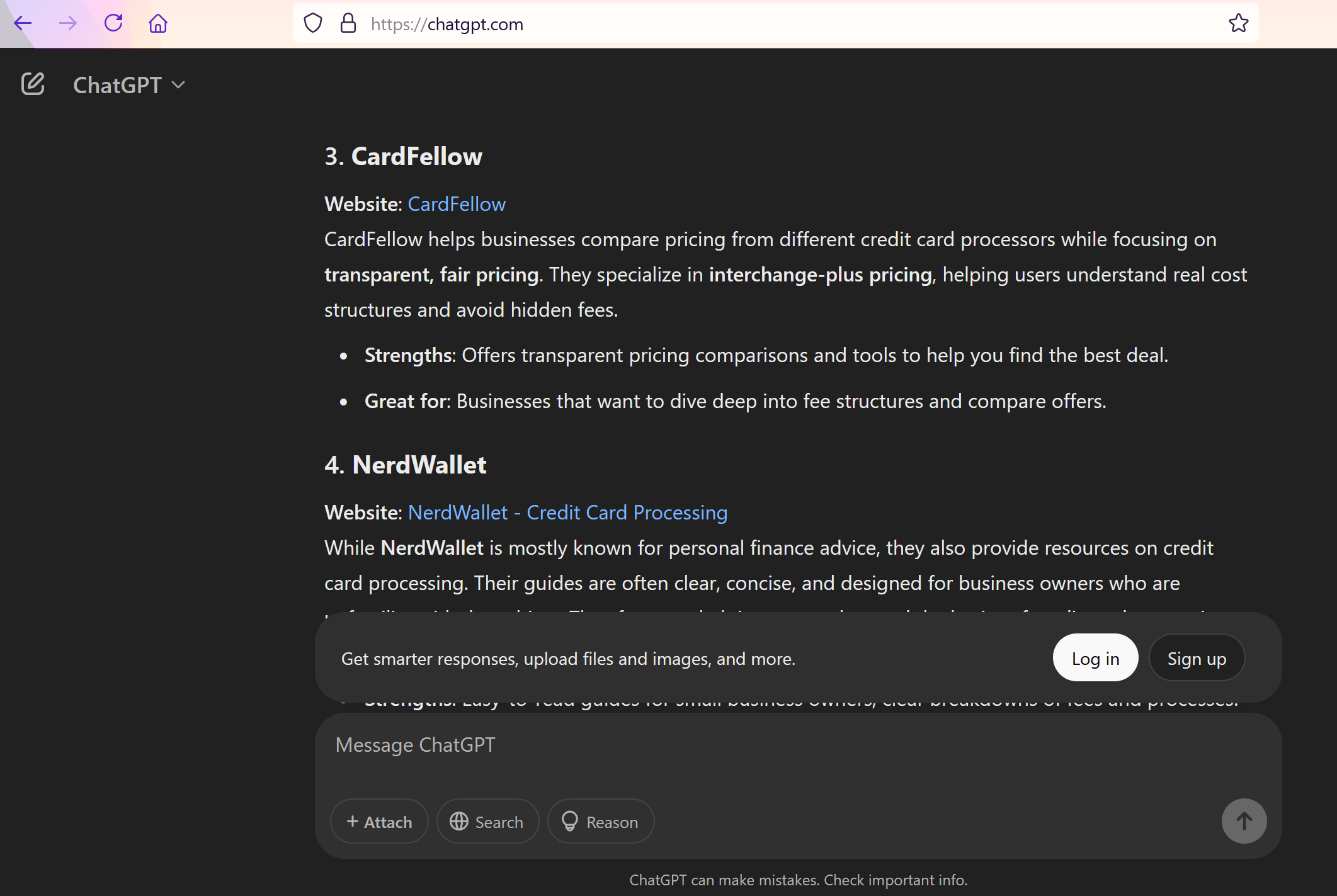

It suggested “commonly considered options” that included Square, PayPal, Stripe and Shopify (flat rate processors) and mentioned “Traditional Merchant Accounts.”

For those accounts, it claims they are best for “businesses with high transaction volume” but doesn’t specify what volume that is. Additionally, it states that fees are “generally lower for high-volume businesses” and adds that fees are “around 0.5% – 2.6% per transaction” without specifying a pricing model.

There are a few things to unpack there. Firstly, 0.5% is lower than the wholesale cost of credit card processing, so it could be referring to just the processor’s markup, which is a common way to express fees for interchange plus pricing. However, many businesses, even those with lower transaction volumes, can secure smaller markups than that.

On the other end of the spectrum, 2.6% is a more typical flat rate pricing model, but that would not be “generally lower for high-volume businesses.” In fact, flat rate pricing is typically more expensive for high-volume businesses. It’s important not to confuse simplicity with low cost.

For this part, ChatGPT is giving information that is correct, but requires you to have existing knowledge to parse.

ChatGPT’s Factors to Consider

After suggesting specific processors, ChatGPT’s response continued. In order to find the cheapest processor, it suggests considering monthly fees, transaction volume, and types of transactions.

Once again, these are good things to consider and do affect your processing costs. Rates and fees vary depending on the type of transaction (in-person, keyed, online, etc.) and monthly fees vary by processor. Transaction volume affects pricing as well.

ChatGPT’s conclusion asked if I would like help comparing specific processors for my needs.

Let’s do it.

Comparing Credit Card Processors with ChatGPT

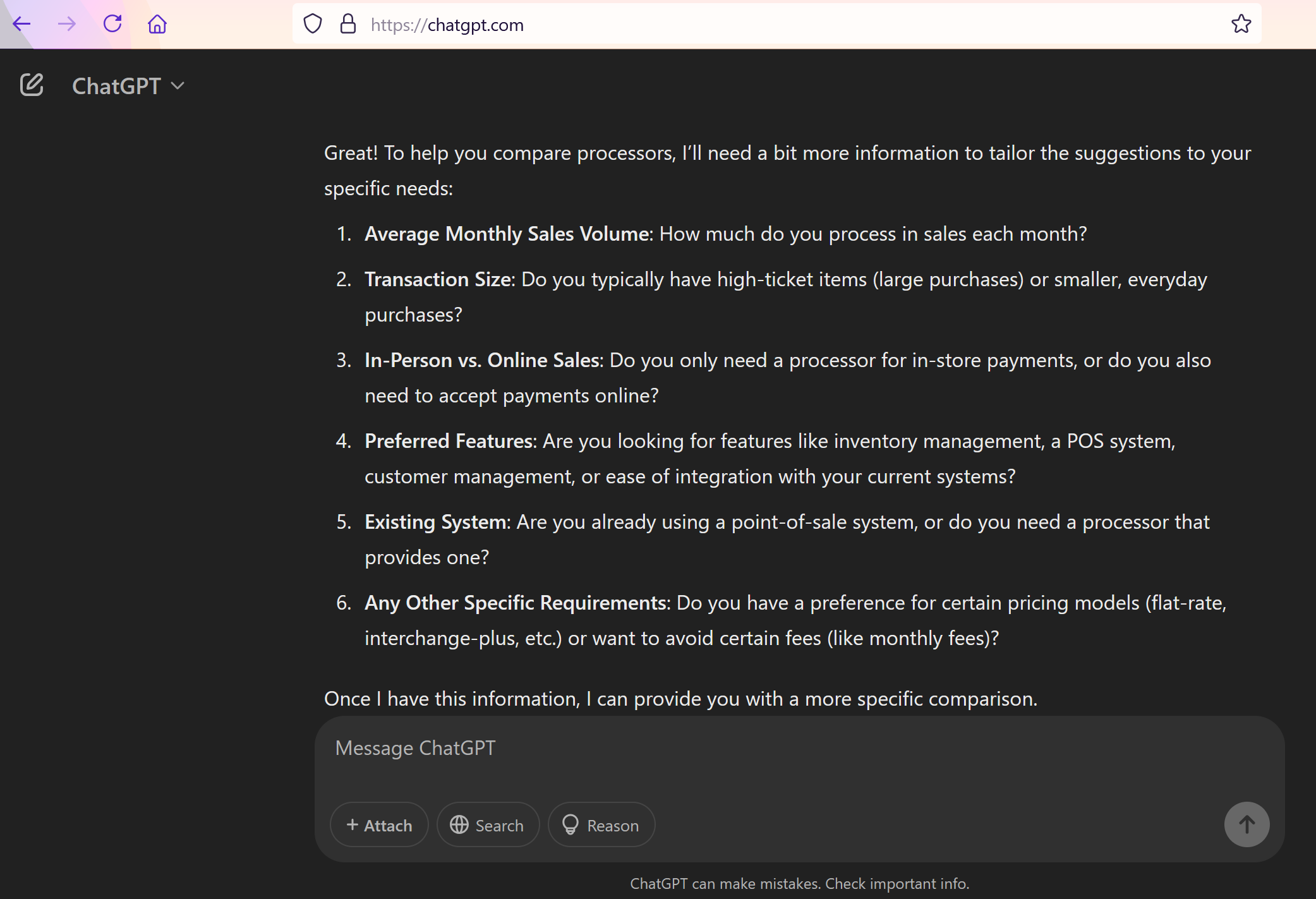

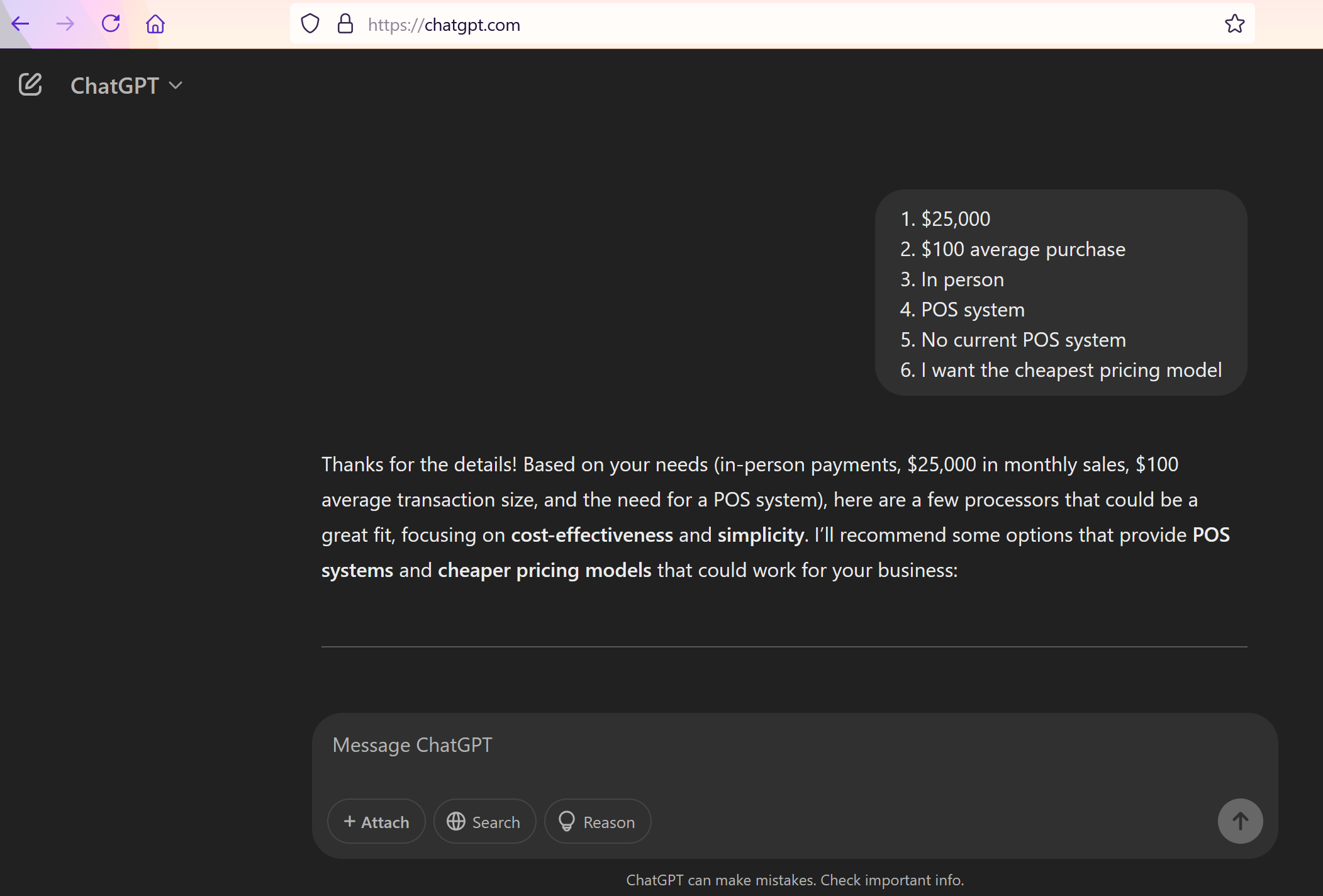

Once I said yes I would like help, ChatGPT immediately responded that it needs more information to tailor answers to my needs. As you can see in the screenshot, it requested six things:

- Average Monthly Sales Volume

- Transaction Size

- In-Person vs. Online Sales

- Preferred Features

- Existing System

- Any Other Specific Requirements

Again, these are great questions that are highly relevant to finding the right credit card processor.

I responded with the following, which I’ll call Scenario A.

- $25,000

- $100 average purchase

- In person

- POS system

- No current POS system

- I want the cheapest pricing model

Armed with my answers, ChatGPT was ready to provide my tailored solutions and I was curious to see how they would compare to suggestions I receive through CardFellow.

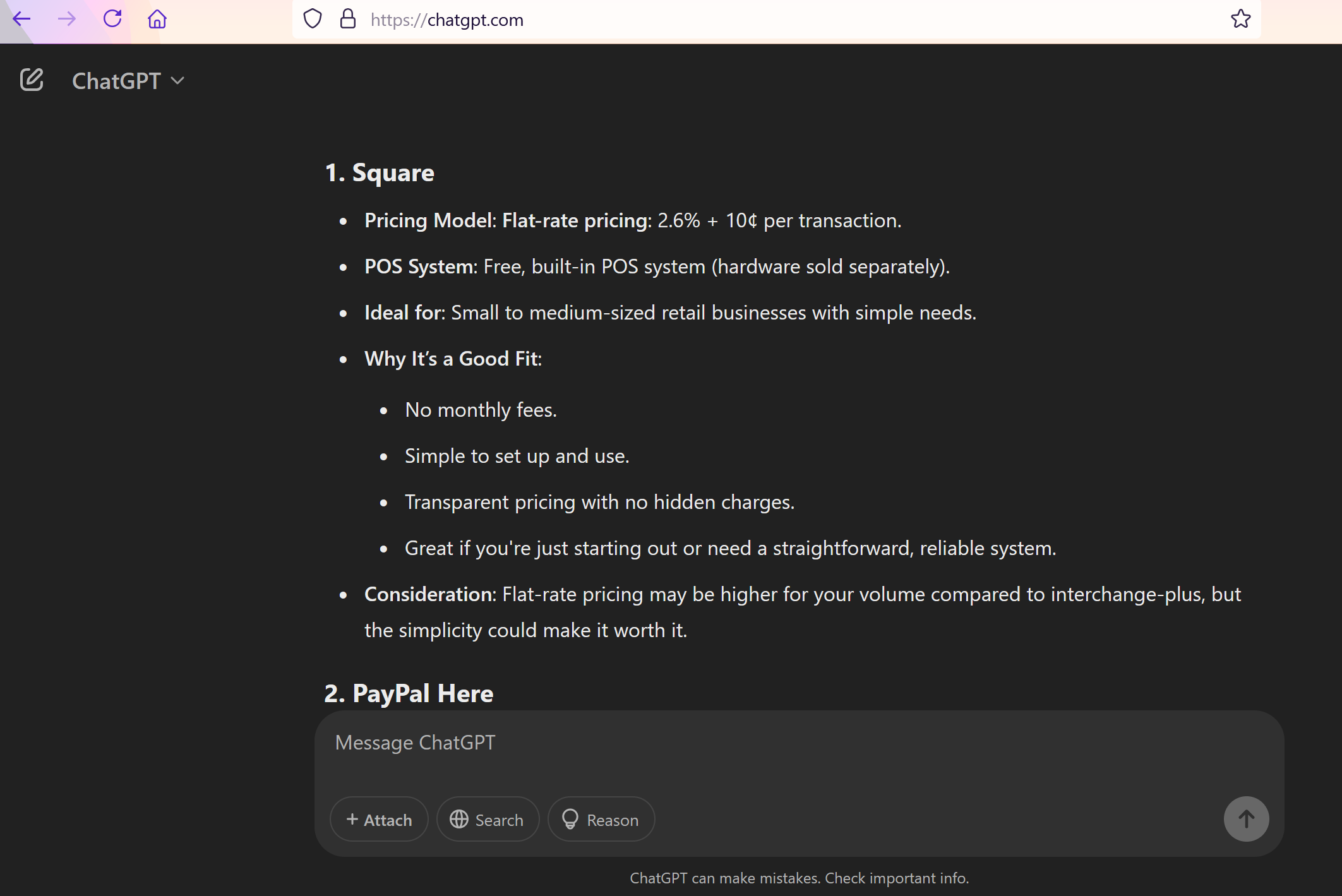

Scenario A

Not a great start.

The first option ChatGPT suggests is Square, which should have been ruled out as the cheapest option given two important details: my average transaction size is $100 and my average monthly volume is $25,000.

Why does that matter?

Square is a flat rate credit card processor, with pricing that appears simple, but is often not the lowest cost. Interestingly, ChatGPT acknowledges that at the end of its suggestion, stating that flat-rate pricing may be higher for my volume compared to interchange plus, but the simplicity could make it worth it.

Nowhere did I indicate that simplicity was a factor for my business; in fact, I explicitly stated that the cheapest pricing model was my answer for question 6 – Other Specific Requirements. In the goal of getting an answer on the cheapest processor for my business, ChatGPT’s first reply is factually incorrect.

How would Square compare to quotes from processors in the CardFellow marketplace for the fictional business in Scenario A? Let’s take a look.

Scenario A: Flat Rate vs. Interchange Plus

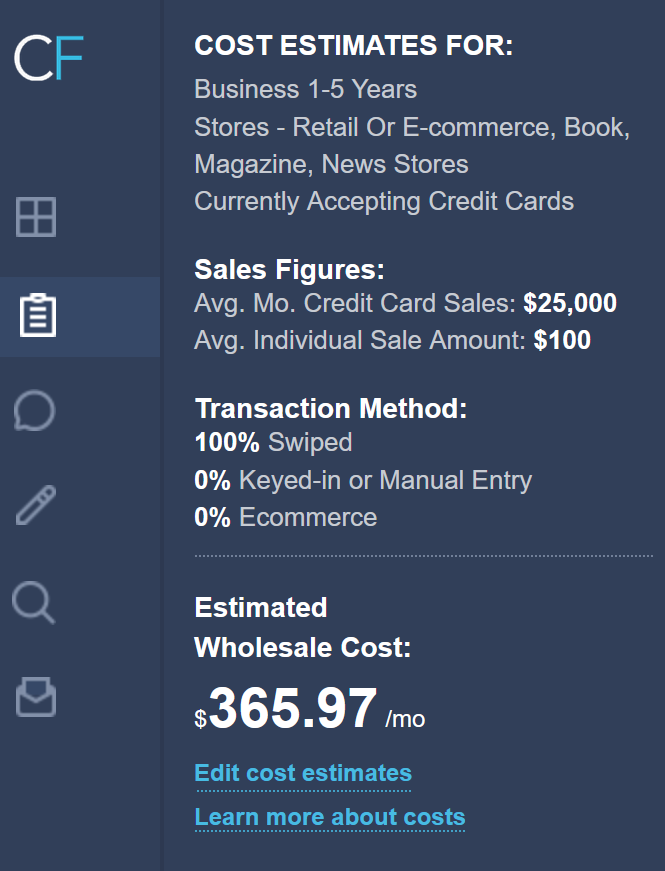

I created a free account at CardFellow entering the details I gave ChatGPT. My fictitious business (a bookstore / retail) processes $25,000 per month in credit card transactions with an average sale of $100. All transactions are in-person (swiped) payments.

CardFellow calculates my estimated wholesale cost (that is, the interchange costs) automatically. I can expect to pay $365.97 in interchange and assessment fees. Note that you’ll always pay those fees; you just won’t see it directly with some pricing models.

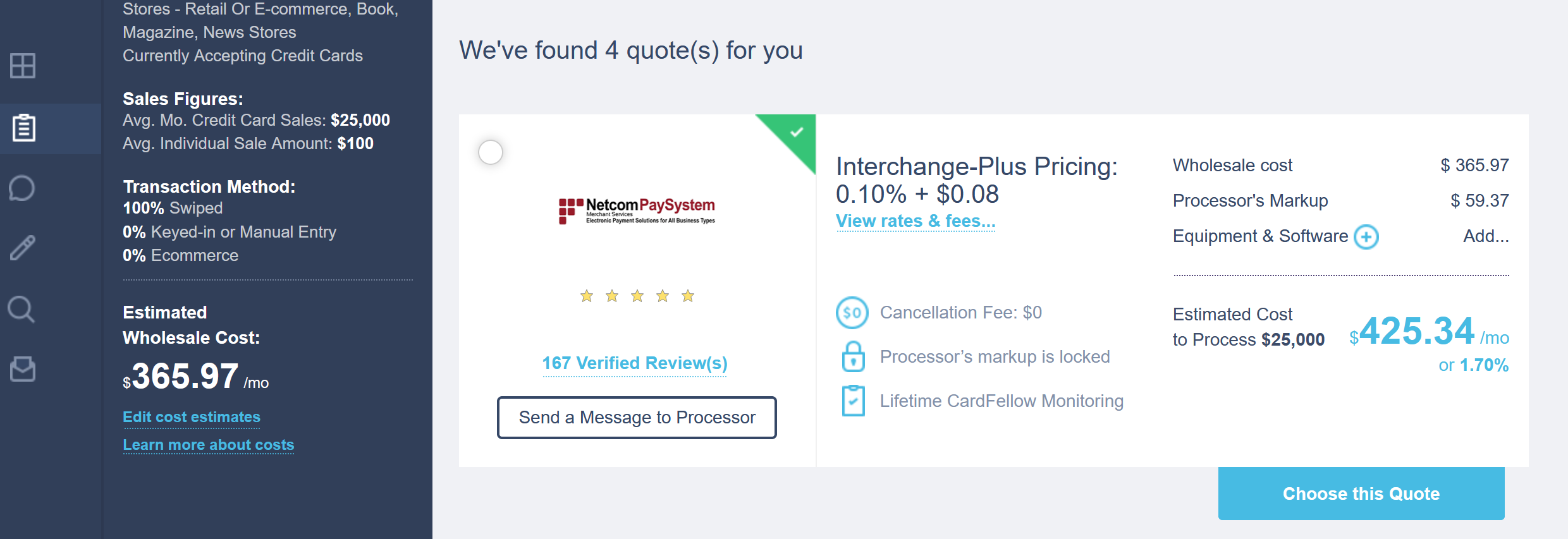

For comparison purposes between two interchange plus quotes, I need to know the processor’s markup. Comparing interchange plus to flat rate is a little trickier, but CardFellow requires processors to fully disclose their fees. So I look for the lowest cost option and find that it’s a company offering me 0.10% and 8 cents per transaction. CardFellow shows that for my transaction size and volume, I can expect to pay $425.34/month with this processor’s quote.

For Square, we can do a little math. We need to know both the percentage total (2.6% of monthly volume) and the number of transactions.

If my business makes $25,000/month and the average sale is $100, we can assume it processes 250 transactions per month.

2.6% of $25,000 = $650

250 transactions x $0.10 = $25

So the total monthly cost for Square will be $675 for my fictional business – approximately $250 more per month than the lowest interchange plus option quoted through CardFellow.

Strike 2, ChatGPT.

Other Suggestions for Scenario A

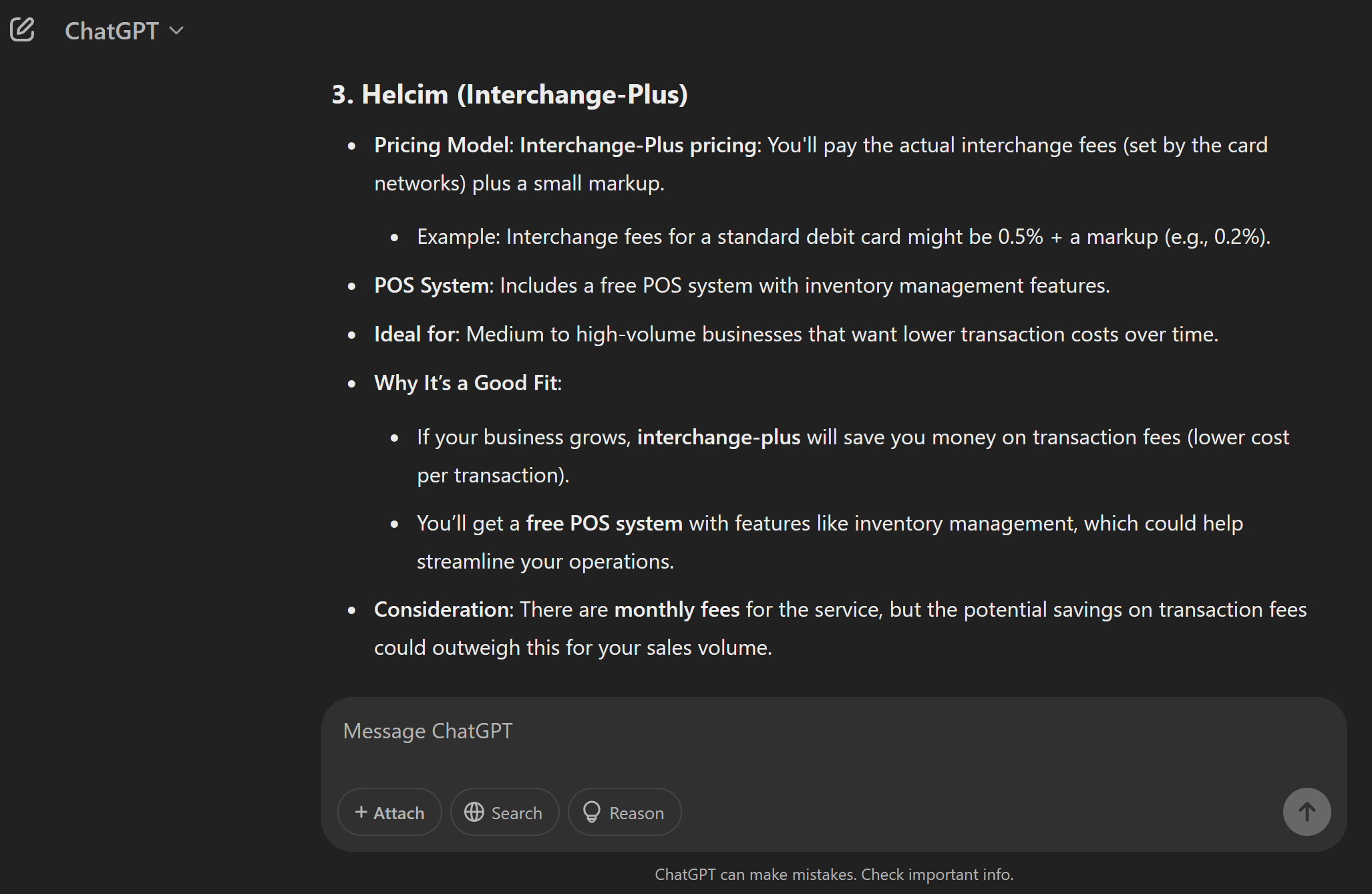

After Square, ChatGPT suggested PayPal Here, another flat rate processor. Its third suggestion is an interchange-plus solution from Helcim, followed by Fattmerchant subscription pricing, and lastly Clover. Since we already discussed flat rate, we will skip explaining PayPal Here. Additionally, since Clover offers both interchange plus and flat rate, we’ll skip that one, as the details for the interchange plus and flat rate explanations would both apply to Clover as well.

Interchange Plus

ChatGPT explains that with interchange plus pricing, I’ll pay the actual interchange fees plus a small markup. This is correct information.

However, it then gets into some confusing statements. First, that it’s ideal for medium- to high-volume businesses that want lower transaction costs over time. Secondly, that “if your business grows, interchange plus will save you money on transaction fees (lowest cost per transaction.)”

I say these are confusing statements because there’s no time delay on savings from an interchange plus pricing model. It’s not just that you’ll have lower transaction costs over time, you’ll have them immediately. The second statement is odd because your business doesn’t need to grow for interchange plus to save you money, either. Consider the math in our Flat Rate vs. Interchange Plus scenario above. The monthly volume and transaction size didn’t change in the comparison math, but the interchange plus scenario is cheaper regardless.

It IS possible to lower pricing with higher volumes, but that can be the case with any pricing model. Even flat rate processors will offer custom rates for businesses with higher volumes. If your business grows, it’s certainly worth keeping an eye on your fees to see if you can negotiate lower. But even if your business doesn’t grow, interchange plus will save you money on transaction fees over other pricing models in many cases.

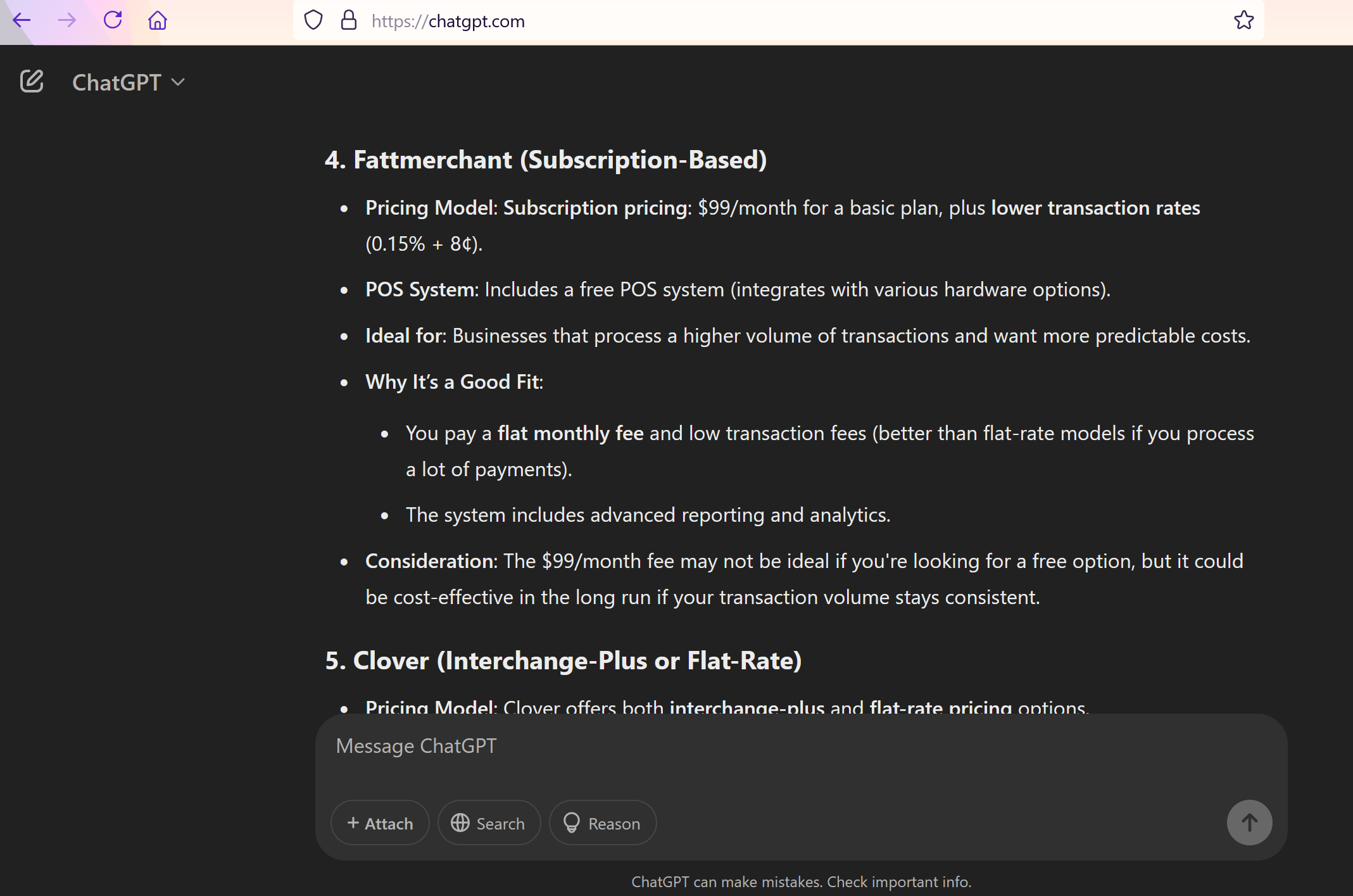

Fattmerchant / Subscription-Based

Right off the bat, we learn that ChatGPT’s answer is at least somewhat out of date; Fattmerchant rebranded in 2021 (the ‘cutoff’ year for ChatGPT’s training) and has gone by the name Stax since then.

However, a subscription model could be a good option for my fictitious business.

One thing I want to highlight here is the difference between “subscription-based” and “interchange plus” pricing models. The truth is, they’re very similar, but subscription pricing tries to market itself as simpler. Some companies, like Stax, claim “0% markup on direct cost interchange.” However, that’s misleading. Any fees charged in addition to the cost of interchange are definitionally a markup, and Stax charges both a monthly fee and a per-transaction cents-based fee. What the company means is that they don’t charge a percentage markup on interchange. Typically, interchange plus will have a percentage markup and a per-transaction cents-based fee; something like 0.2% + 8 cents per transaction. Subscription based pricing will look more like 0% + 10 cents per transaction.

In some cases, the 0% will be more beneficial; in other cases, having a lower cents-based fee is a bigger deal. How do you know when for each? It primarily depends on your transaction size and number of transactions. The rough rule of thumb is that if you have large individual transactions, you’ll want a smaller percentage fee and can accept a larger cents-based fee. For small transactions, you want to minimize the cents-based fee even if there’s a slightly larger percentage. In some cases, it won’t be a very big difference, so it’s worth taking a minute to calculate specifics. Let’s take a look at how the math shakes out for my fictitious business.

Interchange Plus vs. Subscription Pricing

Wholesale costs are the same for all pricing models, so let’s use the wholesale calculation from CardFellow for both: $365.97.

The lowest interchange plus quote in the CardFellow marketplace came out to $425.34. That means that the processor’s markup, including all fees, is $59.37/month. ($425.34 – $365.97)

Therefore, the subscription model must have monthly fees and any transaction fees totaling less than $59.37/month to be more competitive.

The lowest cost Fattmerchant (Stax) monthly plan has a $99/month fee. Without any additional transaction fees, the subscription model by Stax is already more expensive, coming in at $464.97 ($365.97 + $99.) Typical Stax transaction fees range from $0.08 – $0.15. If we assume 8 cents for 250 transactions, the same as the interchange plus solution, that adds $20 for a total of $484.97.)

If the business chooses a plan with a higher monthly fee or if Stax quotes a more expensive transaction fee, the cost difference will be even greater.

However, as you can see, the difference between interchange plus and subscription in this example is much smaller than the difference between interchange plus and flat rate.

Assessing Responses

Overall, I was happy to see that ChatGPT had some factually correct information and was able to ask relevant questions to provide more detail. However, it struggled to give nuanced recommendations that take into account all of the complex factors in something like choosing a credit card processor. In some cases, its answers were not exactly incorrect, but could be misleading or require prior knowledge to fully make sense of what it suggested. For that reason, ChatGPT seems best suited to non-situational, fact-based questions.

Using ChatGPT in credit card processing may be useful but it’s not a silver bullet. AI is great for many things, but it doesn’t yet have the complex reasoning skills of a human expert. It can be a good starting point for learning the basics of a topic or getting direction for where to go for more detailed information, but be careful about trusting it as a sole source of research, especially for anything with variables that are specific to you or your business.

The Problem Even When ChatGPT is Right

There’s one caveat to all of this: even if ChatGPT suggests something that fits the bill, such as Helcim with interchange plus pricing for my fictitious business in Scenario A, there’s an elephant in the room: There’s no guarantee that the processor is actually going to quote you competitively.

Credit card processors are not obligated to offer the same pricing to businesses. This is also what makes credit card processor reviews a minefield.

In addition to the variables we’ve discussed such as industry, average transaction size, and monthly volume, processing reps have leeway to set pricing however they want. That’s why it’s crucial to obtain and thoroughly review a quote you receive for credit card processing. It’s also a good idea to confirm how long that pricing is valid. Ideally, you’ll secure a lifetime rate lock on processor’s markup, which is one of the key benefits of using a service like CardFellow. However, outside of our marketplace, many processors won’t offer such a rate lock. In those situations, at least find out how long your pricing will remain as quoted. Be sure to regularly review it to ensure prices haven’t gone up.

CardFellow clients, we’ll review your pricing for you. Simply give us a call or send over your latest processing statement for your free rate lock review.

Key Takeaways

ChatGPT can be a helpful tool in researching any number of topics that are important to your business, including credit card processing. But there are a few things to remember.

Be careful of potentially outdated information.

ChatGPT does not necessarily have the latest updates for everything. In the case of Fattmerchant, it was still referring to the company by that name instead of Stax; a name change that happened 4 years ago. It’s likely that ChatGPT doesn’t have updated pricing information in some cases as well, since it is not “scraping” the web in real-time.

Your merchant agreement is what matters.

Regardless of what you read from a ChatGPT reply, a processor review, or anywhere else, what’s quoted in your merchant agreement is what matters. Remember, the contract you sign trumps verbal commitments from a processing rep or pricing published on a website or provided by an AI tool.

CardFellow can help.

Our free solution lets you easily compare credit card processors, with the real rates quoted specifically for your business. All quotes include a lifetime rate lock on the processor’s markup and our free statement monitoring service to ensure that your pricing stays locked. Even ChatGPT says we’re your source for expert credit card processing help!