Any business owner that accepts credit cards knows that Visa and Mastercard charge fees for acceptance. But what are those fees, exactly? And are the Visa interchange categories the same as the Mastercard interchange categories?

In this article, we’re going to focus on Visa and Mastercard interchange categories and their effect on your processing fees. In order to do that, we first need to have a common understanding of the basics.

Interchange Basics Refresher

In my article on interchange rates and fees, I mention several times that there are many different interchange “categories,” each with their own rates. If you haven’t read that article yet, it’s a good idea to check that out first as it will give you a better overall understanding of interchange.

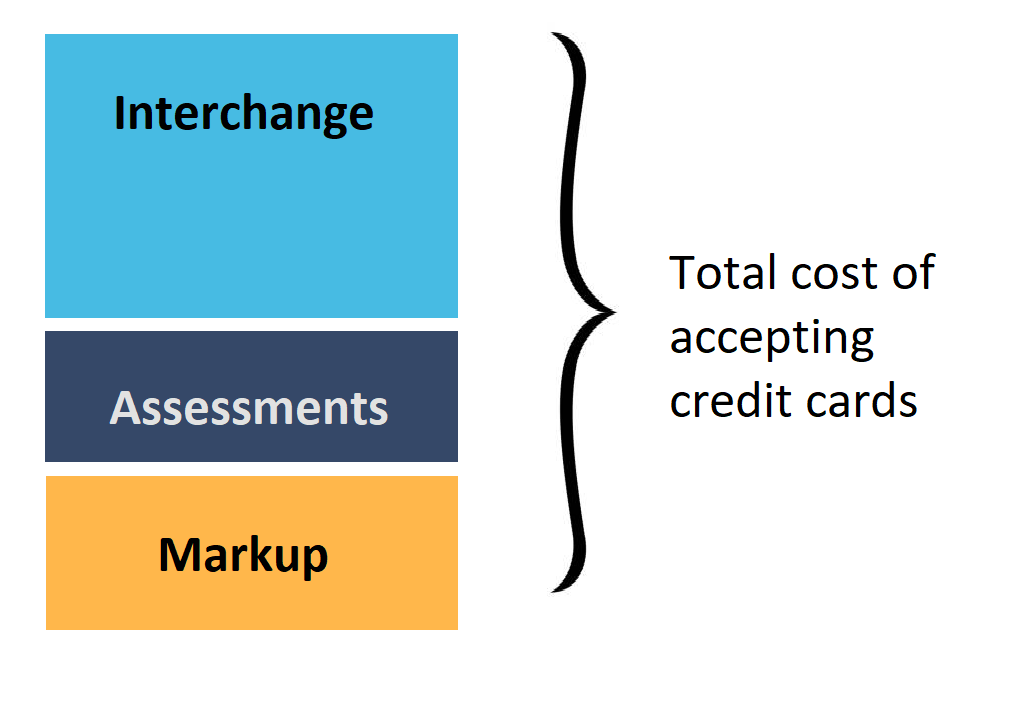

But if you just want a quick overview, here it is: “Interchange” is one of the three core components of credit card processing costs. (Along with “assessments” and processor’s “markup.”)

But interchange isn’t a single rate or fee. As I’ve mentioned, there are hundreds of Visa and Mastercard interchange categories, each with its own rate and fee. Interchange is applied to each individual transaction, meaning that you could have many different categories on your statement. Here is a screenshot of just a few of Visa and Mastercard’s many possible interchange categories.

On top of that, the three categories aren’t an equal part of the total cost. Interchange is the largest. A distribution of the three costs might look more like this:

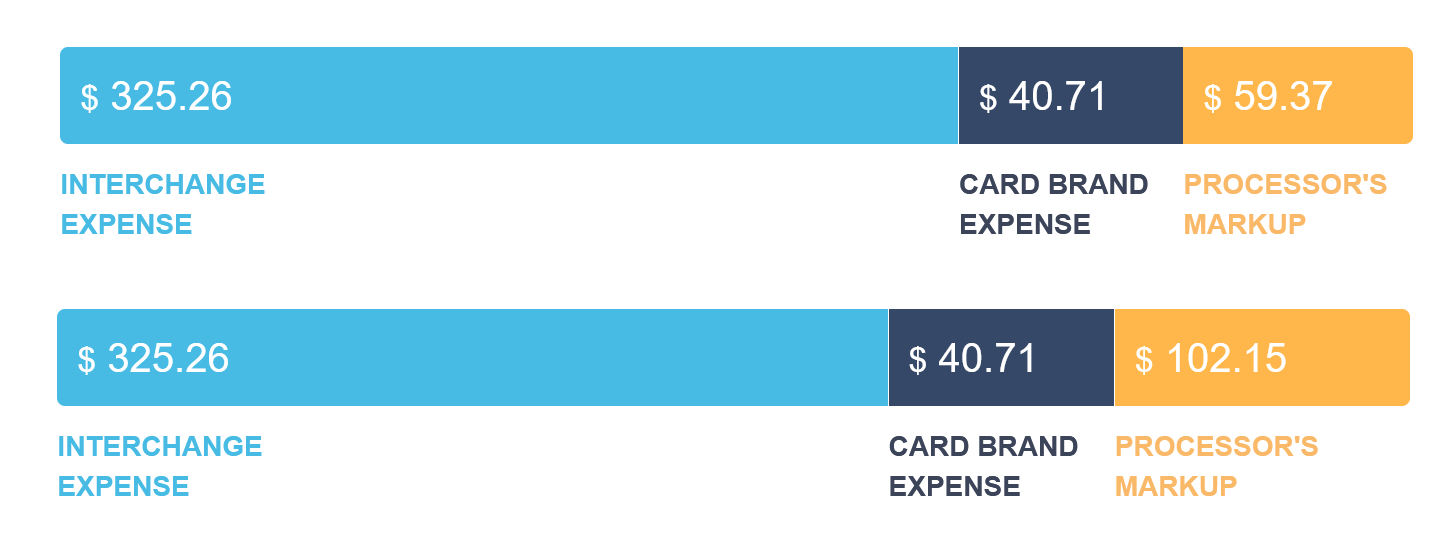

Indeed, this is how we show it to you when you get quotes from processors in CardFellow’s marketplace. In the image below, you can see the quote overview from two different processors for an example business. The light blue interchange bar is the largest, as interchange is the biggest component of cost. This is true even though the second light blue bar is smaller as a proportion of the total cost. The actual interchange is the same, but since the processor in the second quote charges more in markup, interchange is a smaller percentage of the total fees paid. This does not mean interchange is lower, as you can see from the dollar amount. The numbers are exactly the same for interchange and assessments even though the quotes are from different processors.

Interchange Categories

In the larger interchange piece there will be multiple interchange categories, as noted above. Every individual transaction you process will be routed to an interchange category for that transaction.

Of course, not every interchange category applies to every business. We can roughly break them down into four groups: categories that will never apply, categories are unlikely but could apply if certain variables are met, categories that could apply on a per-transaction basis, and common categories.

Let’s break that down a bit.

Categories That Will Never Apply

This is the easiest one. Categories that will never apply are typically industry-specific, and your business is in a different industry. For example, if you own a shoe store, you will never see hotel and car rental interchange categories.

One way that interchange categories are determined is by Merchant Category Code or MCC. Your processor sets your MCC when you sign your merchant agreement, and it doesn’t change. Only certain MCCs are eligible for certain interchange categories. If your MCC is different, you won’t see that interchange category.

Categories That Could Apply, But are Unlikely

This is primarily for volume discounts. Very high volume businesses may be eligible for lower cost interchange categories. However, thresholds start around $1 billion in volume before the categories apply, as you can see from this screenshot of Visa’s performance thresholds.

Common Categories

Common categories are the ones you’ll regularly see on your credit card processing statement. For an average business, you’ll typically see a few dozen interchange categories. We’ll get into some of the most common categories a little later in this article.

It’s important to note here that there are some “common categories” across many types of businesses, but “common” is still relative. There may be categories that are common for you and not for another business. For example, if you accept a lot of corporate cards, seeing interchange categories for corporate cards will be common on your statement, but another business may see them rarely or never.

Categories That Could Apply on a Per-Transaction Basis

Interchange categories that *could* apply on a per-transaction basis are ones that aren’t necessarily common for your business, but appear because of a specific transaction or transactions. This is often a card type you don’t normally see (such as a corporate card or a specific rewards card) or because the transaction didn’t “qualify” for a more common category. In some cases, this indicates an “interchange downgrade” which we’ll get into later.

Qualifying for Interchange Categories

Now that I’ve gone through a refresher on the concept of interchange, how do you know what categories will apply to your business?

As I’ve noted a few times, interchange qualification – meaning which category a transaction will be routed to – happens independently for every transaction. There are multiple factors that affect which category a transaction will go to. Some factors (like your MCC) narrow down the possible interchange categories that will apply, and then other factors (e.g., card type, settlement time) happen on a per-transaction basis to determine the final category.

Main factors that affect the interchange category include: MCC, card type, acceptance method, transaction size, and settlement time. We can roughly think of them as filters that continually narrow down the total possible interchange categories.

Let’s use some hypothetical numbers to illustrate that point. Say there are 200 Visa interchange categories in total. Imagine 100 of them apply to credit cards and 100 apply to debit cards. Now, imagine 50 of the credit card categories are for “card-present” transactions and 50 are for “card-not-present” transactions. Of the 50 card-present categories, imagine 10 of them could apply to retailers, determined by MCC. Those 10 could include things like rewards credit card categories, small ticket categories for purchases under $15.00, corporate card categories, or “downgrade” categories if the transaction doesn’t meet criteria for another category.

The specific factors of the transaction will determine the routing. Once all factors are taken into account, there will only be one category the transaction is charged to. For example, a card-present transaction using a credit card at a retailer for a purchase under $15.00 and settled within 48 hours should qualify for a retail card-present small ticket interchange category. It doesn’t, you may have an interchange downgrade on your hands.

Interchange optimization is the process of ensuring that your transactions are routing to the best possible category, helping minimize the possibility of overpaying (including downgrading) based on preventable factors. Even though you can’t negotiate interchange, there are situations where you can lower your interchange costs by “qualifying” for better categories on a per-transaction basis. You can read more in our article Saving Money with Interchange Optimization.

So if interchange is non-negotiable, why do I have to care about it?

In some cases, you don’t.

If you’re on a pricing model that guarantees passing interchange to you at true cost and you’re confident that your transactions aren’t downgrading to more expensive interchange categories, then deeper exploration into interchange isn’t really necessary.

In practice, many businesses aren’t receiving true pass-through interchange, even when they think they are. There are a few reasons, but the most common are businesses choosing processors with pricing models that conceal interchange (such as flat rate and tiered) or processors engaging in shady practices such as padding interchange.

It’s a good idea to regularly review your transactions to ensure they’re qualifying for the best possible interchange categories. This is one way to ensure you’re not overpaying for credit card processing. If you’re a CardFellow client, be sure to take advantage of our free statement monitoring service that handles this for you. If you’re not a CardFellow client, you can do this yourself, but you’ll need to familiarize yourself with the common interchange categories for your business and learn how to cross-reference what your processor charged vs. what Visa or Mastercard publish for rates. I’ll tackle some “common” categories shortly.

Why doesn’t flat rate pricing use interchange categories?

Some business owners use a processor with flat rate pricing, such as Square, and wonder why they don’t have complex interchange qualification. The truth is, they do, they just don’t show it to you.

Every processing company operates through interchange. The pricing model and transparency of the processor determine whether they show you the interchange categories that applied to your transactions or not. In the case of Square and other flat rate processors, simplicity is key. Instead of showing you interchange (or charging you separately for interchange, assessments, and markup) flat rate processors simply set one rate that they think will be high enough to cover all possible interchange category rates your business could receive. They then just show you the total cost, calculated by the number of transactions you processed times the rates and fees they charge.

It looks simpler, but it’s not always the lowest cost option. This is because you won’t save on the transactions that cost less at interchange than what Square or other flat rate processors charged you. In fact, you won’t even be able to see the interchange categories that applied. For businesses not on a flat rate model, you should be able to review the interchange categories on your statement. Let’s take a look at what you might see.

“Common” Interchange Categories

Remembering the caveat that “common” interchange categories are relative, let’s go through some of the more common categories that we see regularly.

One quick note about debit – we’ll refer to non-regulated debit interchange when discussing fees for common debit categories. Regulated debit interchange is capped at a fixed amount (0.05% + 21 cents per transaction) regardless of other factors. Regulated debit refers to debit transactions using a debit card issued by a bank with $10 billion or more in assets. Unregulated debit is what will have variations in rates and fees.

Visa

- Product 1 and Product 2

- Restaurant 1 and Restaurant 2

- EIRF

- Business Product 1 and Business Product 1

- Non-Qualified

Mastercard

- Merit 1 (Core, Enhanced Value, World, World High Value, World Elite)

- Merit 3 (Core, Enhanced Value, World, World High Value, World Elite)

- Business (Data Rate 1, Data Rate 2)

- Standard

Note: Visa and Mastercard regularly change the names and rates of their interchange categories. This list is not meant to be exhaustive. Be sure to check the latest published Visa and Mastercard interchange tables.